When was the last time a stress test was performed on your group LTD Plan?

When was the last time a stress test was performed on your group LTD Plan?

Employers routinely review medical plans, retirement benefits, and overall compensation strategies.

Yet LTD plans are often left unchanged for years.

Meanwhile, compensation structures, bonus incentives, taxes, and employee financial pressure continue to evolve.

A plan designed years ago may no longer align with how employees are compensated today — especially for highly compensated or incentive-based employees.

A simple income protection analysis can help identify whether current LTD coverage is still keeping pace.

With over 29 years of experience specializing in Supplemental IDI programs, Navis Benefits Group helps employers evaluate income protection strategies and address potential coverage gaps.

Employers routinely review medical plans, retirement benefits, and overall compensation strategies.

Yet LTD plans are often left unchanged for years.

Meanwhile, compensation structures, bonus incentives, taxes, and employee financial pressure continue to evolve.

A plan designed years ago may no longer align with how employees are compensated today — especially for highly compensated or incentive-based employees.

A simple income protection analysis can help identify whether current LTD coverage is still keeping pace.

With over 29 years of experience specializing in Supplemental IDI programs, Navis Benefits Group helps employers evaluate income protection strategies and address potential coverage gaps.

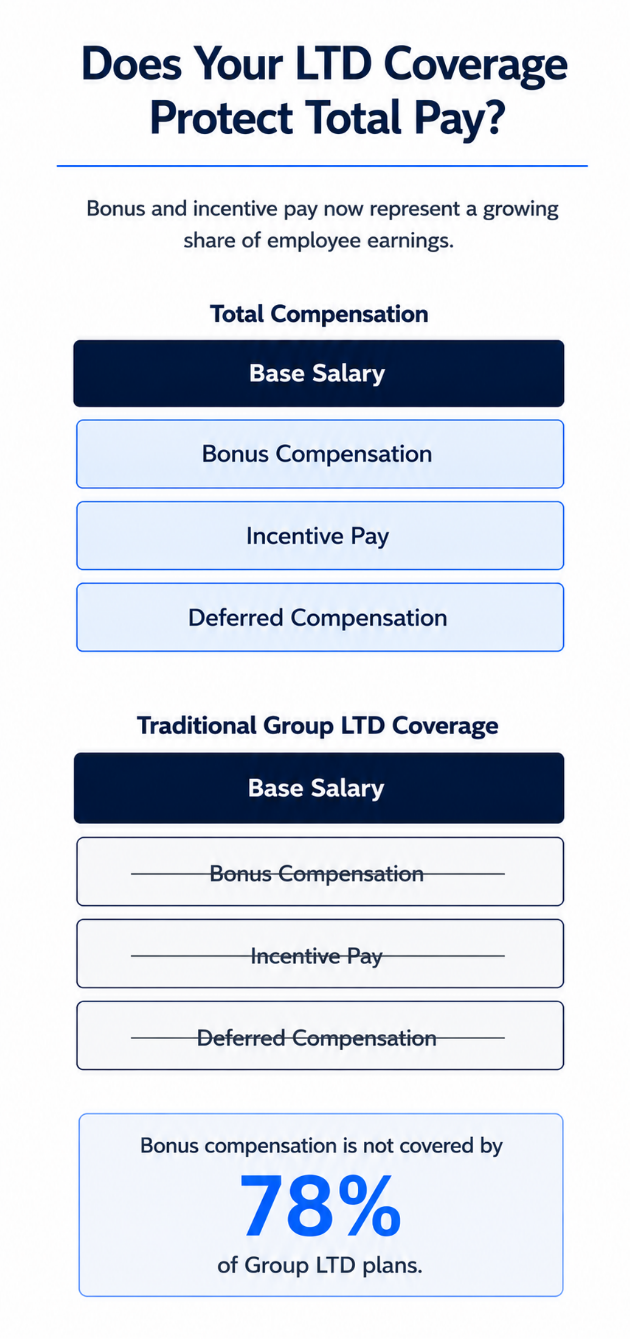

Does your compensation package include bonus or incentive pay?

Does your compensation package include bonuses or incentive pay?

Most Group LTD plans only protect base salary. In fact, bonus compensation is not covered by Group LTD plans 78% of the time.

Meanwhile, bonuses and incentive pay continue to represent a growing share of employee earnings — in some highly compensated professions, over 40% of total pay.

As pay structures evolve, many employers are surprised to learn how much employee income may fall outside traditional LTD coverage.

A simple income protection analysis can help determine whether current LTD coverage still aligns with how employees are paid today.

With over 29 years of experience specializing in Supplemental IDI programs, Navis Benefits Group helps employers evaluate income protection strategies and design solutions to address potential coverage gaps.

Most Group LTD plans only protect base salary. In fact, bonus compensation is not covered by Group LTD plans 78% of the time.

Meanwhile, bonus and incentive pay continue to represent a growing share of employee earnings — in some highly compensated professions, over 40% of total pay.

As pay structures evolve, many employers are surprised to learn how much employee income may fall outside traditional LTD coverage.

A simple income protection analysis can help determine whether current LTD coverage still aligns with how employees are paid today.

With over 29 years of experience specializing in Supplemental IDI programs, Navis Benefits Group helps employers evaluate income protection strategies and design solutions to address potential coverage gaps.

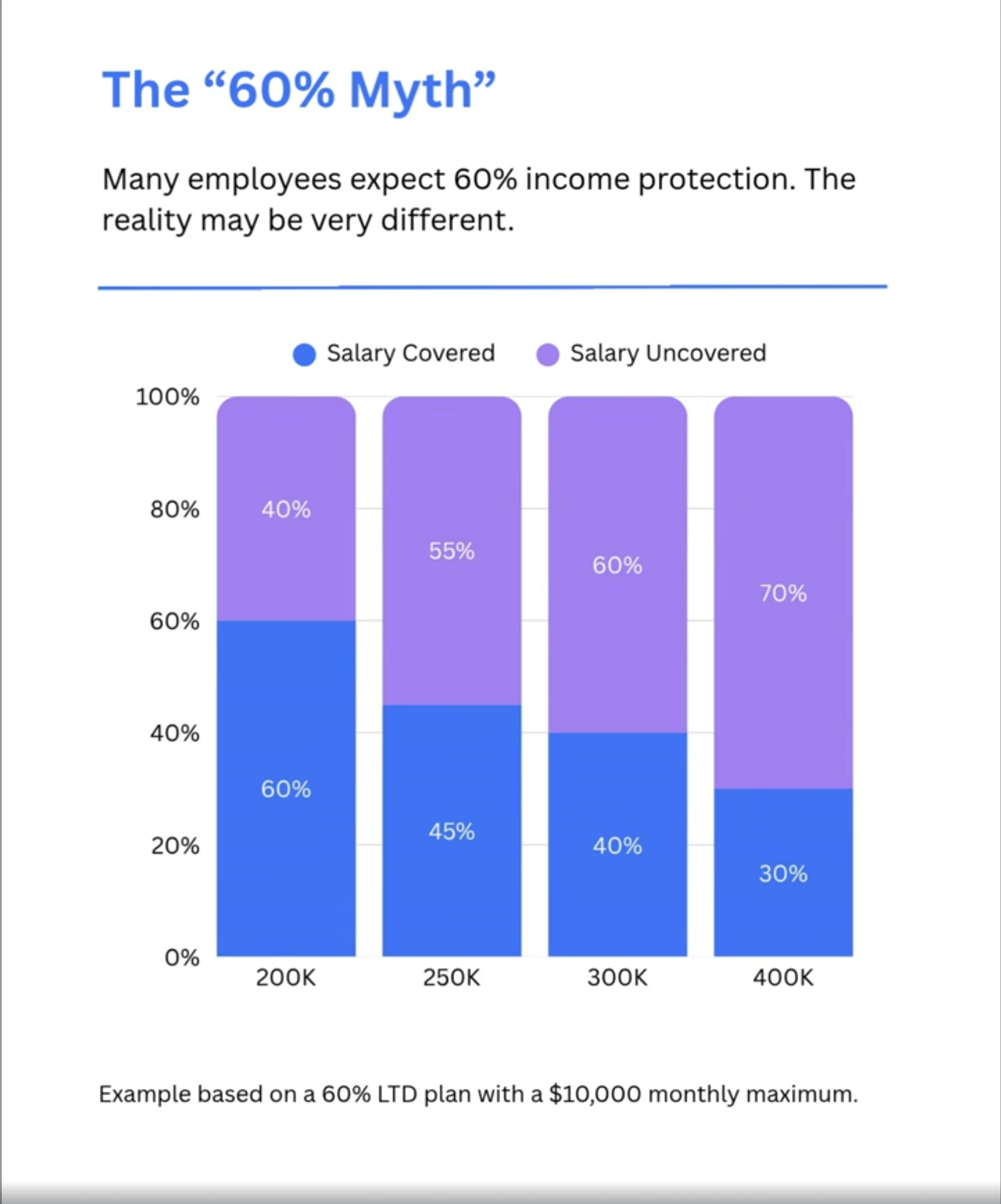

The “60% Myth”

Most employees think they understand their long-term disability (LTD) coverage. The reality is most don’t.

A Group LTD plan intended to replace “60%” of income can look very different once benefits are paid.

Why?

Enter plan maximums, compensation structures, and taxes into the equation, and the actual replacement percentage may be far lower than expected.

Highly compensated employees are bearing the burden of these factors even more than their colleagues.

With over 29 years of experience specializing in Supplemental IDI programs, Navis Benefits Group helps employers design and implement strategies to improve income protection and address potential coverage gaps.

Most employees think they understand their long-term disability (LTD) coverage. The reality is most don’t.

A Group LTD plan intended to replace “60%” of income can look very different once benefits are paid.

Why?

Enter plan maximums, compensation structures, and taxes into the equation, and the actual replacement percentage may be far lower than expected.

Highly compensated employees are bearing the burden of these factors even more than their colleagues.

With over 29 years of experience specializing in Supplemental IDI programs, Navis Benefits Group helps employers design and implement strategies to improve income protection and address potential coverage gaps.

If it’s not broken, don’t fix it!??

If it’s not broken, don’t fix it!??

Many Employers offer a Supplemental Disability (LTD/IDI) plan for their Executives and highly compensated employees. Once implemented, these plans often become stagnant, outdated, and over-priced.

Yes, it’s likely that the Plan Administrator is adding new Executives, terminating old, and exercising the annual benefit coverage increases due to salary increases. It’s not likely, however, that the plan will receive a thorough annual check-up unless the plan is designed and administered by a consultant specializing in Executive Benefit plans.

An Executive Benefit Specialist focuses on these benefits plans, isn’t hostage to the time and energy required by Health Insurance and has a deep understanding of Supplemental Disability programs.

An annual check-up performed by an Executive Benefit Specialist can help ensure the plan still meets the Employer’s financial wellness goals, offers the best pricing, appropriate plan maximum, aligns with the Group LTD plan, includes the best underwriting and Guarantee Issue maximums, and leverages the simplest administrative processes.

You’ve heard the old saying, “If it’s not broken, don’t fix it”. But by avoiding a thorough annual check-up or plan audit, the Supplemental LTD plan will in fact become broken.

Here are three examples:

1. Pricing:

a. The cost of Supplemental Disability plans has decreased significantly over the years. By doing nothing, over the course of just a few years, the Employer is overpaying for the plan – often 20-40% too much. An overhaul of an older plan – one even 5 years old – can deliver significant savings to an employer, despite an aging Executive group.

2. Administration:

a. Supplemental Disability plans normally require simplified underwriting with a short enrollment form. Plans today can be administered without requiring an enrollment form, if the plan is designed with underwriting correctly. Update to a new simplified onboarding process to save Human Resources time - and improve the onboarding experience for Executives.

3. Guarantee Issue Benefit Maximum:

a. A Supplemental Plan installed 5-10 years ago, may no longer adequately protect the Executives’ earnings. With increased earnings over the years, an Executive will eventually “hit” the Supplemental Plan benefit maximum. This means the Executive(s) will receive less than the target income replacement level. Increasing the plan maximum may be necessary.

By partnering with an Executive Disability Benefit Specialist, Employers can save premium, improve the onboarding process, save time, and update the Supplemental Disability Insurance plan to better align with the Employer’s goals.

Navis Benefits Group, LLC, specializes in Supplemental Long-Term Disability Insurance plans. Ask how Navis Benefits Group can help design, market, install, and administer a tailored Supplemental LTD plan.

Many Employers offer a Supplemental Disability (LTD/IDI) plan for their Executives and highly compensated employees. Once implemented, these plans often become stagnant, outdated, and over-priced.

Yes, it’s likely that the Plan Administrator is adding new Executives, terminating old, and exercising the annual benefit coverage increases due to salary increases. It’s not likely, however, that the plan will receive a thorough annual check-up unless the plan is designed and administered by a consultant specializing in Executive Benefit plans. An Executive Benefit Specialist focuses on these benefits plans, isn’t hostage to the time and energy required by Health Insurance and has a deep understanding of Supplemental Disability programs.

An annual check-up performed by an Executive Benefit Specialist can help ensure the plan still meets the Employer’s financial wellness goals, offers the best pricing, appropriate plan maximum, aligns with the Group LTD plan, includes the best underwriting and Guarantee Issue maximums, and leverages the simplest administrative processes.

You’ve heard the old saying, “If it’s not broken, don’t fix it”. But by avoiding a thorough annual check-up or plan audit, the Supplemental LTD plan will in fact become broken.

Here are three examples:

1. Pricing:

a. The cost of Supplemental Disability plans has decreased significantly over the years. By doing nothing, over the course of just a few years, the Employer is overpaying for the plan – often 20-40% too much. An overhaul of an older plan – one even 5 years old – can deliver significant savings to an employer, despite an aging Executive group.

2. Administration:

a. Supplemental Disability plans normally require simplified underwriting with a short enrollment form. Plans today can be administered without requiring an enrollment form, if the plan is designed with underwriting correctly. Update to a new simplified onboarding process to save Human Resources time - and improve the onboarding experience for Executives.

3. Guarantee Issue Benefit Maximum:

a. A Supplemental Plan installed 5-10 years ago, may no longer adequately protect the Executives’ earnings. With increased earnings over the years, an Executive will eventually “hit” the Supplemental Plan benefit maximum. This means the Executive(s) will receive less than the target income replacement level. Increasing the plan maximum may be necessary.

By partnering with an Executive Disability Benefit Specialist, Employers can save premium, improve the onboarding process, save time, and update the Supplemental Disability Insurance plan to better align with the Employer’s goals.

Navis Benefits Group, LLC, specializes in Supplemental Long-Term Disability Insurance plans. Ask how Navis Benefits Group can help design, market, install, and administer a tailored Supplemental LTD plan.

Partner with Navis Benefits Group

Navis Benefits Group’s mission is to give the non-medical benefits the focus, specialization, and shelf space necessary to strengthen the Employee benefits package.

Navis Benefits Group does not work on medical insurance. We focus exclusively on the “other” benefits which often are over-shadowed by Medical Insurance.

We partner with Employee Benefit Firms that focus on medical benefits, as their turn-key outsourced specialty benefits partner, to bring creative non-medical benefit solutions to their Employer clients. We help Employers upgrade their employee benefit plans to state of the art, unique, competitive benefit programs.

With over 29 years of experience in specialty benefit solutions, we pride ourselves in being a partner to our clients, customizing solutions unique to their business and employee benefit needs.

Happy 4th Birthday, Navis Benefits Group!

Today we celebrate Navis Benefits Group’s 4th Birthday, and those that helped make this dream a reality!

I am humbled, and beyond grateful for the support and partnerships that helped make my dream a reality!

Thank you to the Employers and Employee Benefit Firms that chose to partner with Navis Benefits Group and placed their trust and confidence in my firm. And thank you to my carrier partners and vendors, for the support, tools, and extra effort you’ve given to my firm.

A very special thanks to my wife Christina, and my three boys (Dominic, Brayden, and Desmond), for the sacrifices and support you’ve given me along the way. You have been my inspiration and motivation to make Navis Benefits Group a well-respected, and successful firm. Navis Benefits Group is a reflection of you - and of your love and support!

After a successful 25-year career working for one of the industry’s best insurance carriers, making the move to start my own firm was a risky, and frightful proposition to say the least. But it was a dream that I had long wanted to pursue.

I am proud to report on this 4th Birthday, that Navis Benefits Group continues to exceed growth expectations. We’ve successfully helped Employers secure up to 50% savings on ancillary (Group STD/LTD/Life) benefit programs, installed high caliber Supplemental Disability Insurance Programs, Executive Benefit Plans, Long-Term Care Plans; helped Employer’s consolidate Voluntary Worksite Benefit plans; and implemented unique Employee Engagement and New Hire Orientation Platforms. Navis Benefits Group is in a strong position, and proud to celebrate this milestone achievement with our partners, customers, friends, and family.

I will always hold close to my heart, the support, encouragement, guidance and advice of my former colleagues, business partners, employee benefit consultants, human resource professionals, and friends. And most importantly, my family for taking the leap of faith, and for the sacrifices they made in the initial years to get things going!

With Sincere Thanks,

Jamie Reidy

Managing Partner & Founder

Navis Benefits Group is a “specialty benefits” Firm, focusing exclusively on non-medical employee benefits to include Group STD/LTD/Life Benefits, Executive Supplemental Disability Insurance, Voluntary Supplemental Disability Insurance, Executive Life Insurance, Long Term Care Insurance, Voluntary Worksite Benefits, New Hire Orientation Onboarding, and Benefits Enrollment/Communication solutions.

Today we celebrate Navis Benefits Group’s 4th Birthday, and those that helped make this dream a reality!

I am humbled, and beyond grateful for the support and partnerships that helped make my dream a reality!

Thank you to the Employers and Employee Benefit Firms that chose to partner with Navis Benefits Group and placed their trust and confidence in my firm. And thank you to my carrier partners and vendors, for the support, tools, and extra effort you’ve given to my firm.

A very special thanks to my wife Christina, and my three boys (Dominic, Brayden, and Desmond), for the sacrifices and support you’ve given me along the way. You have been my inspiration and motivation to make Navis Benefits Group a well-respected, and successful firm. Navis Benefits Group is a reflection of you - and of your love and support!

After a successful 25-year career working for one of the industry’s best insurance carriers, making the move to start my own firm was a risky, and frightful proposition to say the least. But it was a dream that I had long wanted to pursue.

I am proud to report on this 4th Birthday, that Navis Benefits Group continues to exceed growth expectations. We’ve successfully secured up to 50% savings on ancillary (Group STD/LTD/Life) benefit programs, installed high caliber Supplemental Disability Insurance Programs, Executive Benefit Plans, Long-Term Care Plans; helped Employer’s consolidate Voluntary Worksite Benefit plans; and implemented unique Employee Engagement and New Hire Orientation Platforms. Navis Benefits Group is in a strong position, and proud to celebrate this milestone achievement with our partners, customers, friends, and family.

I will always hold close to my heart, the support, encouragement, guidance and advice of my former colleagues, business partners, employee benefit consultants, human resource professionals, and friends. And most importantly, my family for taking the leap of faith, and for the sacrifices they made in the initial years to get things going!

With Sincere Thanks,

Jamie Reidy

Managing Partner & Founder

Navis Benefits Group is a “specialty benefits” Firm, focusing exclusively on non-medical employee benefits to include Group STD/LTD/Life Benefits, Executive Supplemental Disability Insurance, Voluntary Supplemental Disability Insurance, Executive Life Insurance, Long Term Care Insurance, Voluntary Worksite Benefits, New Hire Orientation Onboarding, and Benefits Enrollment/Communication solutions.

Haven’t Marketed Your Supplemental Disability Insurance Plan Lately?

Employers, do you offer a Supplemental Long-Term Disability Insurance plan as a benefit? If you do, congratulations! You are in a class of Employers that believes in offering a strong benefits package, to reward your key employees.

You’ve recognized that Group LTD alone can’t fully address the income requirements of your highly compensated employees. You understand risk diversification is an effective tool in your disability benefit strategy. And you offer a strong benefits program, to reward your most valued employees.

But when was the last time you completed a thorough review or marketing of your Supplemental Disability Insurance plan? You review your health insurance, STD/LTD/Life, and possibly your voluntary benefits, at least every other year. So, why not review and market your Supplemental Disability Insurance plan?

Yes, most Supplemental Disability plans employ a “non-can” rate structure. This means that the products rates are filed with the State(s) DOI and can’t be increased for any reason. In addition, the insurance carrier can’t cancel the individual contracts/policies which make up the benefit plan, for any reason. But, the Employer, and the Employees, are not bound to this “non-can” provision, and can terminate the coverage at any time.

Why would an Employer want to cancel, or replace, a Supplemental Disability Insurance plan? Some reasons include securing more competitive pricing, modernizing benefit plan provisions, negotiate a higher Guarantee Issue maximum, streamlining enrollment/new hire onboarding process, and leveraging improved administrative efficiencies.

Pricing – savings between 20% to 50% from current premium.

Increase benefit maximum/guarantee issue amount.

To ensure protection levels are keeping up with rising incomes and inflation.

Audit coverage:

Covered compensation: does your plan cover bonus compensation, commission, and K-1 earnings, in addition to base salary?

Definition of disability – does it align with your industry, and how your employees are paid? Is a loss of earnings required, or not?

Benchmark plan design against peers

Modernize benefit provisions, to include:

Mental/Nervous/Drug/Alcohol Protection for Full Benefit Duration

Removal of the 24-month limitation, so disabilities caused by mental/nervous/drug/alcohol are treated like “any other disability”

Long-term Care protection during the working years

Enhanced Paid Family Leave protection to care for family members

Serious Illness/Critical Illness protection helps with out-of-pocket expenses for disabilities resulting from a heart attack, cancer, or stroke.

NO Pre-existing condition limitation

Recovery Benefit continues benefit payments when an employee returns to work full-time following a disability but still experiences an income loss.

Important protection for employees that are paid commission or bonus income or are accounts receivable occupations (i.e. attorneys).

Process Improvements: onboard new eligible employees via census enrollment.

The days of collecting individual enrollment applications are over.

Guaranteed Standard Issue (GSI) vs. Guarantee Issue (GI)

GSI: 180 Day Active at Work requirement, which could result in an employee decline.

GI: Remove the 180 Day Active at Work requirement and replace it with a 1 Day Active at Work requirement, to align with Group STD/LTD/Life.

Navis Benefits Group specializes in Supplemental Disability Insurance Programs. With 29 years of specializing in Supplemental Disability Programs, including 25 years as an Executive Disability Insurance Consultant for the #1 provider of Supplemental Disability Insurance plans, Jamie is well positioned to assist you in the marketing of your current program. He’s worked with Fortune 500 Companies, Top AM 100 Law Firms, large Healthcare Organizations, Financial Institutions, and small professional employer organizations to achieve significant savings, process improvements, and benefit enhancements. Reach out to Navis Benefits Group, for a complete review of your Supplemental Disability Insurance plan.

Employers, do you offer a Supplemental Long-Term Disability Insurance plan as a benefit? If you do, congratulations! You are in a class of Employers that believes in offering a strong benefits package, to reward your key employees.

You’ve recognized that Group LTD alone can’t fully address the income requirements of your highly compensated employees. You understand risk diversification is an effective tool in your disability benefit strategy. And you offer a strong benefits program, to reward your most valued employees.

But when was the last time you completed a thorough review or marketing of your Supplemental Disability Insurance plan? You review your health insurance, STD/LTD/Life, and possibly your voluntary benefits, at least every other year. So, why not review and market your Supplemental Disability Insurance plan?

Yes, most Supplemental Disability plans employ a “non-can” rate structure. This means that the products rates are filed with the State(s) DOI and can’t be increased for any reason. In addition, the insurance carrier can’t cancel the individual contracts/policies which make up the benefit plan, for any reason. But, the Employer, and the Employees, are not bound to this “non-can” provision, and can terminate the coverage at any time.

Why would an Employer want to cancel, or replace, a Supplemental Disability Insurance plan? Some reasons include securing more competitive pricing, modernizing benefit plan provisions, negotiate a higher Guarantee Issue maximum, streamlining enrollment/new hire onboarding process, and leveraging improved administrative efficiencies.

Pricing – savings between 20% to 50% from current premium.

Increase benefit maximum/guarantee issue amount.

To ensure protection levels are keeping up with rising incomes and inflation.

Audit coverage:

Covered compensation: does your plan cover bonus compensation, commission, and K-1 earnings, in addition to base salary?

Definition of disability – does it align with your industry, and how your employees are paid? Is a loss of earnings required, or not?

Benchmark plan design against peers

Modernize benefit provisions, to include:

Mental/Nervous/Drug/Alcohol Protection for Full Benefit Duration

Removal of the 24-month limitation, so disabilities caused by mental/nervous/drug/alcohol are treated like “any other disability”

Long-term Care protection during the working years

Enhanced Paid Family Leave protection to care for family members

Serious Illness/Critical Illness protection helps with out-of-pocket expenses for disabilities resulting from a heart attack, cancer, or stroke.

NO Pre-existing condition limitation

Recovery Benefit continues benefit payments when an employee returns to work full-time following a disability but still experiences an income loss.

Important protection for employees that are paid commission or bonus income or are accounts receivable occupations (i.e. attorneys).

Process Improvements: onboard new eligible employees via census enrollment.

The days of collecting individual enrollment applications are over.

Guaranteed Standard Issue (GSI) vs. Guarantee Issue (GI)

GSI: 180 Day Active at Work requirement, which could result in an employee decline.

GI: Remove the 180 Day Active at Work requirement and replace it with a 1 Day Active at Work requirement, to align with Group STD/LTD/Life.

Navis Benefits Group specializes in Supplemental Disability Insurance Programs. With 29 years of specializing in Supplemental Disability Programs, including 25 years as an Executive Disability Insurance Consultant for the #1 provider of Supplemental Disability Insurance plans, Jamie is well positioned to assist you in the marketing of your current program. He’s worked with Fortune 500 Companies, Top AM 100 Law Firms, large Healthcare Organizations, Financial Institutions, and small professional employer organizations to achieve significant savings, process improvements, and benefit enhancements. Reach out to Navis Benefits Group, for a complete review of your Supplemental Disability Insurance plan.

The 80% Step-Up

The 80% Step-up: Upgrade Your Group LTD

Employers should consider updating their long-term disability program to provide 75%-80% replacement of total compensation, to better help employees avoid financial devastation during a disability.

Studies show that the American worker has been financially struggling for a long time.It is no secret. Even a “full paycheck” - 100% of base and bonus - is no longer enough to pay the bills.

Most Employers’ Group Long-Term Disability (LTD) Insurance plans only protect up to 60% of base salary. Replacing 60% of base salary was the “standard plan design”, once upon a time. Since the American worker cannot meet financial obligations with 100% of total compensation – protecting only 60% of base salary is no longer adequate.

Why not simply enhance the Group LTD plan? An employer could explore a Group LTD solution. However, Employers will find that despite the best efforts, a Group LTD plan that replaces 75% or 80% of total compensation does not exist.

In addition, addressing other shortfalls inherent to Group LTD plans, such as including total compensation, offering a higher benefit maximum to better protect highly compensated employees, and offering a tax-free benefit creates a high-risk LTD plan profile that would be extremely expensive. Group LTD carriers are conservative with offering these plan enhancements, especially when bundled. Never mind a plan design with 75% or 80% replacement of total compensation.

Many Fortune 500 companies have revised their long-term disability programs to include supplemental long-term disability insurance plans. These Supplemental plans can help protect up to 80% of base and bonus income when layered on top of Group LTD. Supplemental plans cannot protect 100% of income. Doing so would invite significant anti-selection according to the actuaries. But 80% is permissible and provides better protection than the “standard plan”.

Supplemental plans leverage non-can rates (fixed, state-filed rates) that cannot change for any reason, with group-like premiums. And since Supplemental claims experience has no negative impact on Group LTD claims experience or pricing, Supplemental plans in a sense serve as Group LTD’s version of “stop loss.”

Navis Benefits Group, LLC, specializes in Supplemental Long-Term Disability Insurance plans. Ask how Navis Benefits Group can help design, market, install, and administer a tailored Supplemental LTD plan

Upgrade Your Group LTD

Employers should consider updating their long-term disability program to provide 75%-80% replacement of total compensation, to better help employees avoid financial devastation during a disability.

Studies show that the American worker has been financially struggling for a long time. It is no secret. Even a “full paycheck” - 100% of base and bonus - is no longer enough to pay the bills.

Many Employers’ Group Long-Term Disability (LTD) Insurance plans only protect up to 60% of base salary. Replacing 60% of base salary was the “standard plan design”, once upon a time. Since the American worker cannot meet financial obligations with 100% of total compensation – protecting only 60% of base salary is no longer adequate.

Why not simply enhance the Group LTD plan? An employer could explore a Group LTD solution. However, Employers will find that despite the best efforts, a Group LTD plan that replaces 75% or 80% of total compensation does not exist.

In addition, addressing other shortfalls inherent to Group LTD plans, such as including total compensation, offering a higher benefit maximum to better protect highly compensated employees, and offering a tax-free benefit creates a high-risk LTD plan profile that would be extremely expensive. Group LTD carriers are conservative with offering these plan enhancements, especially when bundled. Never mind a plan design with 75% or 80% replacement of total compensation.

Many Fortune 500 companies have revised their long-term disability programs to include supplemental long-term disability insurance plans. These Supplemental plans can help protect up to 80% of base and bonus income when layered on top of Group LTD. Supplemental plans cannot protect 100% of income. Doing so would invite significant anti-selection according to the actuaries. But 80% is permissible and provides better protection than the “standard plan”.

Supplemental plans leverage non-can rates (fixed, state-filed rates) that cannot change for any reason, with group-like premiums. And since Supplemental claims experience has no negative impact on Group LTD claims experience or pricing, Supplemental plans in a sense serve as Group LTD’s version of “stop loss.”

Navis Benefits Group, LLC, specializes in Supplemental Long-Term Disability Insurance plans. Ask how Navis Benefits Group can help design, market, install, and administer a tailored Supplemental LTD plan.

The “Oops” Moment

The “Oops” Moment

When Benefits Professionals Drop the Ball: Executive Employment Agreements and Disability Insurance

In the hustle and bustle of managing employee benefits, a key component of an Executive Employment Agreement is often overlooked, leaving an Employer exposed to a significant financial liability, and potential legal liability.

Read on, to find out where and how Employers, Plan Administrators, and Employee Benefit Consultants miss the mark, and why this is such an important topic.

But first, what is an Executive Employment Agreement, and why should Plan Administrators be concerned?

An Executive Employment Agreement is a formal contract that outlines the terms and conditions of an executive's employment. These agreements include information about:

Salary

Benefits

Stock options or awards.

Vacation time allotment.

Responsibilities

Compensation

Termination clauses.

Competition and confidentiality.

Executive Employment Agreements commonly include the guarantee of disability insurance:

· During employment

· Up to 60%, without a monthly cap on benefits

· Often required to protect total compensation

· That in the event of a corporate “change in control” of ownership, merger/acquisition, or Executive termination, that the Employer continue to provide and pay for the same level of disability insurance for a specified period.

The key component of the Executive Employment Agreement often overlooked is the guarantee of disability insurance to replace a percentage of income (ex: 60% to 100% replacement) without a monthly benefit maximum.

Most Employers offer Group Long Term Disability (LTD) insurance. So, what is the issue?

Group LTD by itself often cannot meet the requirements outlined in the Executive Employment Agreement. Here is how:

1. LTD plans include monthly benefit maximums, which limit the amount of coverage paid per month.

a. These maximums result in a lower income replacement level, for highly compensated employees.

b. Agreements do not include a benefit maximum. A guarantee of 60% means just that; it is not subject to a monthly benefit maximum like LTD.

2. LTD plans only cover salary 78% of the time, by design. But the Agreement may require that total compensation be protected.

3 . LTD plans are not truly portable. This means that upon the Executive’s termination, due to a change in control/acquisition, the Employer cannot provide the Executive disability insurance as promised. LTD plans are convertible, not portable. Conversion permits terminated employees to convert the Group contract into a very restrictive individual contract. The conversion requires medical underwriting, and the cost of coverage is expensive. Moreover, the converted coverage typically provides protection for a limited time, and the contractual definitions are a shell of what LTD provides. Last, most Executive Employment Agreements will guarantee disability insurance for up to 2 years, even if the Executive has secured another opportunity.

Case Study - Fortune 500 Company:

a. 250 SVPs earn between $300,000 - $2,000,000 of base salary.

b. Target bonus of 30%

c. Group LTD covers 60% of the salary, to a monthly maximum of $15,000.

i. This protects salaries up to $300,000 at 60%.

1. Salaries over $300,000 receive less than 60% due to the $15,000/month maximum.

ii. Group LTD does not cover bonus compensation.

d. The Executive Employment Agreement for the 250 Executives requires that:

i. 60% of total compensation is to be paid in the event of a disability.

1. No monthly maximum stated.

ii. In the event of termination due to a merger/acquisition, the Company must pay for Disability Insurance, providing the same 60% replacement, for 2 years after termination.

e. Two Issues:

1. Group LTD does not achieve 60% replacement:

a. LTD monthly benefit maximum limits protection

b. LTD does not cover bonus compensation.

Example:

An Executive earning a salary of $500,000 + a bonus of $150,000, or $650,000 in total compensation, only has 28% of total compensation protected. This Executive requires $32,500 on monthly benefit, but would only receive $15,000 from the Group LTD.

2. Group LTD is not truly portable.

a. Therefore, the Company would need to “self-insure” the risk in the event of an Executive termination due to a change in control (merger/acquisition).

These two issues may require self-insurance, potentially affecting the balance sheet. IRS accounting rules (for C-Corp, FASB 112), require the employer to set aside appropriate reserves for a claim, when self-insuring the claim.

In the example above (Executive earning $650,000), if the Executive were employed while disabled, the LTD would pay $15,000. The employer would be contractually obligated to pay $17,500/month ($32,500 -$15,000). The reserve for a $17,500/month claim, might be $1,750,000, using a reserve factor of 100 as an example. This reserve must be reported on the Company’s balance sheet according to FASB 112.

Now, imagine the Executive was terminated due to a merger. The Company does not have portable coverage to offer, so self-insures the agreed promise to pay for 60% protection, for 2 years after termination. Remember, the agreement was to “pay” for coverage, but the Company needs to self-insure in the absence of a portable product. The benefit duration of the claim could be much longer, such as 5 years, or the Normal Retirement Age. The Executive goes on claim a year after termination. The Company is now obligated to pay $32,500/month, for the duration of the claim. Thereserve and corresponding impact to the balance sheet would be substantial, for an Executive that is no longer employed by the Company.

Further, the Company must make determinations whether to pay a claim, since there is no insurance company providing guidance or advice to pay. With precedent now set, what is the Company pays this claim and mistakenly fails to pay another claim with similar (or different) merits. This creates a possible legal liability.

You may be wondering, why would an Employer include language in the Executive Employment Contract, promising coverage upon termination due to a change in control? Good question. But it happens, and it is often aligned with other promised benefits.

True Story – Fortune 500 Case Study:

I received a phone call from an Employee Benefit Consultant, asking if I could assist her in providing portable individual disability insurance to 100 or so Executives, as they were just terminated due to an acquisition. Unfortunately for the Company, the ships had already sailed on that option. Insurance carriers do not offer coverage to unemployed Executives. Even if they did, the coverage would have required full medical underwriting (good luck with that!) and been extremely expensive.

We were able to help rectify this exposed gap for the 250 SVPs and above, moving forward, however. But the challenge could not be met by upgrading Group LTD alone.

· Group LTD carriers provided a higher monthly limit, but the limits were still insufficient to cover the total compensation for most executives.

· Further, a super high maximum, on an experienced rated employer (fully credible claims experience due to the large number of covered employees and experience years), would create sizable reserve exposure and future LTD pricing spikes in the event of a high benefit max claim.

· Group LTD is not portable, so the Agreement’s requirement to offer coverage upon termination due to change in control/acquisition, could not be solved with LTD.

Rather, the gap was solved with a restructured Group LTD plan, coupled with Supplemental Disability Insurance, and Excess High-Risk coverage. Both the Supplemental and Excess coverages were secured with deeply discounted rates, on a Guaranteed Issue Basis, and included true portability at the same rates. Further, the claims experience on the Supplemental and Excess coverages would not negatively impact on the Group LTD claims/reserves, serving as a “stop-loss.” Last, although the portable coverage only protected approximately 30% of total compensation, it also served to provide direction to the Company in making claims determination for the self-insured portion; like an “advice to pay”. This helped limit the Company’s legal liability, in determining when to pay the self-insured portion by following the guidance of the Supplemental and Excess coverages.

Plan Administrators, and Benefit Professionals, should investigate what disability insurance and income replacement requirements are specified in their Company’s key Executives’ Employment Contracts. Chances are you might be surprised, and you will discover that the current Group LTD plan alone does not meet the requirements.

Navis Benefits Group, LLC, can help you address the gaps presented by Executive Employment Agreements, by assisting in the design, and installation, of Supplemental and Excess Disability Insurance Solutions. With over 29 years of experience in specialty benefit solutions, we pride ourselves in being an ally and partner to our clients, customizing solutions unique to their business and employee benefit needs.

James Reidy

Managing Partner

Navis Benefits Group, LLC

860-462-6408

JReidy@NavisBenefitsGroup.com

NavisBenefitsGroup.com

The “Oops” Moment

When Benefits Professionals Drop the Ball: Executive Employment Agreements and Disability Insurance

In the hustle and bustle of managing employee benefits, a key component of an Executive Employment Agreement is often overlooked, leaving an Employer exposed to a significant financial liability, and potential legal liability.

Read on, to find out where and how Employers, Plan Administrators, and Employee Benefit Consultants miss the mark, and why this is such an important topic.

But first, what is an Executive Employment Agreement, and why should Plan Administrators be concerned?

Salary

Benefits

Stock options or awards.

Vacation time allotment.

Responsibilities

Compensation

Termination clauses

Competition and confidentiality.

Executive Employment Agreements commonly include the guarantee of disability insurance:

During employment

Up to 60%, without a monthly cap on benefits

Often required to protect total compensation

That in the event of a corporate “change in control” of ownership, merger/acquisition, or Executive termination, that the Employer continue to provide and pay for the same level of disability insurance for a specified period.

The key component of the Executive Employment Agreement often overlooked is the guarantee of disability insurance to replace a percentage of income (ex: 60% to 100% replacement) without a monthly benefit maximum.

Most Employers offer Group Long Term Disability (LTD) insurance. So, what is the issue?

Group LTD by itself often cannot meet the requirements outlined in the Executive Employment Agreement. Here is how:

1. LTD plans include monthly benefit maximums, which limit the amount of coverage paid per month.

a. These maximums result in a lower income replacement level, for highly compensated employees.

b. Agreements do not include a benefit maximum. A guarantee of 60% means just that; it is not subject to a monthly benefit maximum.

2. LTD plans only cover salary 78% of the time, by design. But the Agreement may require that total compensation be protected.

3. LTD plans are not truly portable. This means that upon the Executive’s termination, due to a change in control/acquisition, the Employer cannot provide the Executive disability insurance as promised. LTD plans are convertible, not portable. Conversion permits terminated employees to convert the Group contract, to a very restrictive individual contract. The conversion required medical underwriting, and the cost of coverage is expensive. Moreover, the converted coverage typically provides protection for a limited timeframe, and the contractual definitions are a shell of what LTD provides. Last, most Executive Employment Agreements will guarantee disability insurance for up to 2 years, even if the Executive has secured another opportunity. Conversion doesn’t solve the problem of portable coverage.

Case Study - Fortune 500 Company:

250 SVPs earn between $300,000 - $2,000,000 of base salary.

Target bonus of 30%

Group LTD covers 60% of the salary, to a monthly maximum of $15,000.

This protects salaries up to $300,000 at 60%. Salaries over $300,000 receive less than 60% due to the $15,000/month maximum.

Group LTD does not cover bonus compensation.

The Executive Employment Agreement for the 250 Executives requires that:

60% of total compensation is to be paid in the event of a disability. No monthly maximum stated.

In the event of termination due to a merger/acquisition, the Company must pay for Disability Insurance, providing the same 60% replacement, for 2 years after termination.

Two Issues:

Group LTD does not achieve 60% replacement:

LTD monthly benefit maximum limits protection

LTD does not cover bonus compensation.

Example:

An Executive earning a salary of $500,000 + a bonus of $150,000, or $650,000 in total compensation, only has 28% of total compensation protected. This Executive requires $32,500 on monthly benefit, but would only receive $15,000 from the Group LTD.

2. Group LTD is not truly portable.

Therefore, the Company would need to “self-insure” the risk in the event of an Executive termination due to a change in control (merger/acquisition).

These two issues may require self-insurance, potentially affecting the balance sheet. IRS accounting rules (for C-Corp, FASB 112), require the employer to set aside appropriate reserves for a claim, when self-insuring the claim.

In the example above (Executive earning $650,000), if the Executive were employed while disabled, the LTD would pay $15,000. The employer would be contractually obligated to pay $17,500/month ($32,500 -$15,000). The reserve for a $17,500/month claim, might be $1,750,000, using a reserve factor of 100 as an example. This reserve must be reported on the Company’s balance sheet according to FASB 112.

Now, imagine the Executive was terminated due to a merger. The Company does not have portable coverage to offer, so self-insures the agreed promise to pay for 60% protection, for 2 years after termination. Remember, the agreement was to “pay” for coverage, but the Company needs to self-insure in the absence of a portable product. The benefit duration of the claim could be much longer, such as 5 years, or the Normal Retirement Age. The Executive goes on claim a year after termination. The Company is now obligated to pay $32,500/month, for the duration of the claim. The reserve and corresponding impact to the balance sheet would be substantial, for an Executive that is no longer employed by the Company.

Further, the Company must make determinations on whether to pay a claim, since there is no insurance company providing guidance or advice to pay. With precedent now set, what is the Company pays this claim and mistakenly fails to pay another claim with similar (or different) merits. This creates a possible legal liability.

You may be wondering, why would an Employer include language in the Executive Employment Contract, promising coverage upon termination due to a change in control? Good question. But it happens, and it is often aligned with other promised benefits.

True Story – Fortune 500 Case Study:

I received a phone call from an Employee Benefit Consultant, asking if I could assist her in providing portable individual disability insurance to 100 or so Executives, as they were just terminated due to an acquisition. Unfortunately for the Company, the ships had already sailed on that option. Insurance carriers do not offer coverage to unemployed Executives. Even if they did, the coverage would have required full medical underwriting (good luck with that!) and been extremely expensive.

We were able to help rectify this exposed gap for the 250 SVPs and above, moving forward, however. But the challenge could not be met by upgrading Group LTD alone.

Group LTD carriers provided a higher monthly limit, but the limits were still insufficient to cover the total compensation for most executives.

Further, a super high maximum, on an experienced rated employer (fully credible claims experience due to the number of covered employees and experience years), would create sizable reserve exposure and future LTD pricing spikes in the event of a high benefit max claim.

Group LTD is not portable, so the Agreement’s requirement to offer coverage upon termination due to change in control/acquisition, could not be solved with LTD.

Rather, the gap was solved with a restructured Group LTD plan, coupled with Supplemental Disability Insurance, and Excess High-Risk coverage. Both the Supplemental and Excess coverages were secured with deeply discounted rates, on a Guaranteed Issue Basis, and included true portability at the same rates. Further, the claims experience on the Supplemental and Excess coverages would not negatively impact on the Group LTD claims/reserves, serving as a “stop-loss.” Last, although the portable coverage only protected approximately 30% of total compensation, it also served to provide direction to the Company in making claims determination for the self-insured portion; like an “advice to pay”. This helped limit the Company’s legal liability, in determining when to pay the self-insured portion by following the guidance of the Supplemental and Excess coverages.

Plan Administrators, and Benefit Professionals, should investigate what disability insurance and income replacement requirements are specified in their Company’s key Executives’ Employment Contracts. Chances are you might be surprised, and you will discover that the current Group LTD plan alone does not meet the requirements.

Navis Benefits Group, LLC, can help you address the gaps presented by Executive Employment Agreements, by assisting in the design, and installation, of Supplemental and Excess Disability Insurance Solutions. With over 29 years of experience in specialty benefit solutions, we pride ourselves in being an ally and partner to our clients, customizing solutions unique to their business and employee benefit needs.

James Reidy

Managing Partner

Navis Benefits Group, LLC

860-462-6408

JReidy@NavisBenefitsGroup.com

NavisBenefitsGroup.com

Why Offer Supplemental Disability Insurance (IDI)?

Most employers offer Group Long Term Disability (LTD) insurance to protect their employees’ incomes and lifestyles.

While Group LTD provides a good foundation for protecting the income of most employees, highly compensated employees often remain underinsured, and financially exposed in the event of a disability. Why?

Monthly LTD benefit maximum limits coverage

LTD does not typically protect bonus compensation.

Employer-paid LTD is taxable at time of claim.

Owners/Partners: LTD may not protect W-2 or K-1 income.

How Does a Supplemental Disability Insurance (IDI) Plan Work?

Supplemental IDI provides an additional monthly benefit, layered on top of the Group LTD benefit. This benefit is offered to employees on a Guarantee Issue (GI) basis, like Group LTD. Coverage is typically paid for by the Employer and generally costs less than 1% of the covered employees’ combined payroll. For larger Employers, coverage can be offered on a payroll deduction basis. In addition:

IDI premiums are deeply discounted, providing “group-like” rates.

Unlike Group LTD rates, Supplemental IDI rates are fixed, locking in at purchase age.

IDI coverage is fully portable, at the same rate.

The “Benefits” of Supplemental IDI

Supplemental IDI plans can further enhance your top performers’ benefit package, by:

Improving income protection with a higher aggregate benefit amount

Providing up to 80% income replacement

Protecting bonus compensation, and other forms of income such as K-1 income

Meeting the requirements of an Executive’s Employment Agreement, which often requires 60%+ income protection.

Note that LTD alone often can’t meet this requirement due to monthly benefit maximums.

Types of Companies are Good Candidates for Supplemental IDI Coverage

Companies in certain industries tend to be more likely buyers of Supplemental IDI, such as law firms, physician groups, financial institutions, professional firms, pharmaceutical and manufacturing companies. However, most companies with 5 or more employees earning over $100,000 are strong candidates.

While over 50% of Fortune 500 Companies offer Supplemental IDI, smaller companies also offer Supplemental IDI. In fact, 75% of Supplemental IDI plans sold cover 7-10 highly compensated employees.

Navis Benefits Group, LLC, is a leading provider of Supplemental Disability Insurance programs. With over 29 years of experience specializing in Supplemental IDI programs, Navis can help you design, install, and administer an effective and affordable Supplemental IDI plan.

Most employers offer Group Long Term Disability (LTD) insurance to protect their employees’ incomes and lifestyles.

While Group LTD provides a good foundation for protecting the income of most employees, highly compensated employees often remain underinsured, and financially exposed in the event of a disability. Why?

Monthly LTD benefit maximum limits coverage

LTD does not typically protect bonus compensation.

Employer-paid LTD is taxable at time of claim.

Owners/Partners: LTD may not protect W-2 or K-1 income.

How Does a Supplemental Disability Insurance (IDI) Plan Work?

Supplemental IDI provides an additional monthly benefit, layered on top of the Group LTD benefit. This benefit is offered to employees on a Guarantee Issue (GI) basis, like Group LTD. Coverage is typically paid for by the Employer and generally costs less than 1% of the covered employees’ combined payroll. For larger Employers, coverage can be offered on a payroll deduct basis. In addition:

IDI premiums are deeply discounted, providing “group-like” rates.

Unlike Group LTD rates, Supplemental IDI rates are fixed, locking in at purchase age.

IDI coverage is fully portable, at the same rate.

The “Benefits” of Supplemental IDI

Supplemental IDI plans can further enhance your top performers’ benefit package, by:

Improving income protection with a higher aggregate benefit amount

Providing up to 80% income replacement

Protecting bonus compensation, and other forms of income such as K-1 income

Meeting the requirements of an Executive’s Employment Agreement, which often requires 60%+ income protection.

Note that LTD alone, often can’t meet this requirement due to monthly benefit maximums.

Types of Companies are Good Candidates for Supplemental IDI Coverage

Companies in certain industries tend to be more likely buyers of Supplemental IDI, such as law firms, physician groups, financial institutions, professional firms, pharmaceutical and manufacturing companies. However, most companies with 5 or more employees earning over $100,000 are strong candidates. While over 50% of Fortune 500 Companies offer Supplemental IDI, smaller companies also offer Supplemental IDI. In fact, 75% of Supplemental IDI plans sold cover 7-10 highly compensated employees.

Navis Benefits Group, LLC, is a leading provider of Supplemental Disability Insurance programs. With over 29 years of experience specializing in Supplemental IDI programs, Navis can help you design, install, and administer an effective and affordable Supplemental IDI plan.

Not Offering This Benefit, Yet?

Not Offering This Benefit, Yet?

Most employers already offer Supplemental Life Insurance, on a voluntary basis for all employees, or on an employer-paid basis for Executives. But surprisingly, only about half of Fortune 500 Companies offer Supplemental Disability Insurance Plans.

Why, given that the American worker has a 4 x greater likelihood of becoming disabled, versus dying, during the working years?

One reason may be perceptions. With some exploration, these perceptions are truly misperceptions. Here are two common misperceptions:

1. Enrollment/Guarantee Issue:

o Misperception:

Supplemental Voluntary Group Life is easy to enroll, since it is offered on a Guaranteed Issue basis. Supplemental Disability Insurance is hard to enroll and not offered on a Guaranteed Issue basis.

o Truth:

Supplemental Disability Insurance is easier than ever to enroll. With the right negotiation, it can be offered on a Guaranteed Issue basis, or Guarantee Standard Issue basis, making enrollment easy.

Often, Employer-paid Supplemental Disability Insurance can be enrolled just like Employer-paid Group LTD – via a census.

Voluntary Supplemental IDI can be enrolled via a web platform, which includes decision-making support and a personalized illustration. Communication and educational support can be provided by an Executive Benefit Specialty Broker, in conjunction with the carrier. The “employer lift” is minimal. This product is typically offered “off-cycle” from the health insurance/open enrollment period.

2. Cost:

o Misperception:

Supplemental Life Insurance is inexpensive. Supplemental Disability Insurance is extremely expensive.

o Truth:

Supplemental Disability Insurance is very affordable, often costing less than 1% of compensation. Carriers offer deeply discounted premiums, resulting in group-like pricing. Today’s benefit, offered through the employer, is very affordable, sometimes less than Group LTD.

Supplemental Disability Insurance can be offered on an Employer-paid basis, or on a Voluntary Basis.

Employer-paid Executive Supplemental Disability Insurance often costs a fraction of a cost compared to employer-paid Supplemental Executive Life Insurance.

Group Long-Term Disability (LTD) insurance provides a good foundation for income protection, in the event of a disability. However, Group LTD plans inherently have limitations in protection levels, and present gaps in coverage.

Simply put, Group LTD protection does not provide enough protection by itself. Benefit maximums leave highly compensated employees under-protected (less than the plan’s target protection level); common forms of compensation such as bonus, are not covered in 78% of LTD plans; and benefits are often taxable at time of claim.

Even if the common LTD plan’s target replacement level of 60% is achieved, 60% replacement still results in an income shortfall during a disability. With higher medical expenses incurred during a disability, coupled with the higher cost of living in today’s inflationary environment, consider offering a Supplemental Disability Insurance plan that can protect up to 75% or 80% of pre-disability earnings.

Supplemental Disability Insurance can cover total compensation, is fully portable, offered on a Guarantee Issue basis, easy to install, can be employer-paid or voluntary, and is a very affordable benefit.

May is Disability Insurance Awareness Month (DIAM), and it is a suitable time to explore offering this benefit program.

Navis Benefits Group, LLC specializes in Supplemental Disability Insurance plans, and can help you design, market, install, and administer the plan.

Not Offering This Benefit, Yet?

Most employers already offer Supplemental Life Insurance, on a voluntary basis for all employees, or on an employer-paid basis for Executives. But surprisingly, only about half of Fortune 500 Companies offer Supplemental Disability Insurance Plans. Why, given that the American worker has a 4 x greater likelihood of becoming disabled, versus dying, during the working years?

One reason may be perceptions. With some exploration, these perceptions are truly misperceptions. Here are two common misperceptions:

1. Enrollment/Guarantee Issue:

o Misperception:

Supplemental Voluntary Group Life is easy to enroll, since it is offered on a Guaranteed Issue basis. Supplemental Disability Insurance is hard to enroll and not offered on a Guaranteed Issue basis.

o Truth:

Supplemental Disability Insurance is easier than ever to enroll. With the right negotiation, it can be offered on a Guaranteed Issue basis, or Guarantee Standard Issue basis, making enrollment easy.

Often, Employer-paid Supplemental Disability Insurance can be enrolled just like Employer-paid Group LTD – via a census.

Voluntary Supplemental IDI can be enrolled via a web platform, which includes decision-making support and a personalized illustration. Communication and educational support can be provided by an Executive Benefit Specialty Broker, in conjunction with the carrier. The “employer lift” is minimal. This product is typically offered “off-cycle” from the health insurance/open enrollment period.

2. Cost:

o Misperception:

Supplemental Life Insurance is inexpensive. Supplemental Disability Insurance is extremely expensive.

o Truth:

Supplemental Disability Insurance is very affordable, often costing less than 1% of compensation. Carriers offer deeply discounted premiums, resulting in group-like pricing. Today’s benefit, offered through the employer, is very affordable, sometimes less than Group LTD.

Supplemental Disability Insurance can be offered on an Employer-paid basis, or on a Voluntary Basis.

Employer-paid Executive Supplemental Disability Insurance often costs a fraction of a cost compared to employer-paid Supplemental Executive Life Insurance.

Group Long-Term Disability (LTD) insurance provides a good foundation for income protection, in the event of a disability. However, Group LTD plans inherently have limitations in protection levels, and present gaps in coverage. Simply put, Group LTD protection does not provide enough protection by itself.

Group LTD benefit maximums leave highly compensated employees under-protected (less than the plan’s target protection level); common forms of compensation such as bonus, are not covered in 78% of LTD plans; and benefits are often taxable at time of claim. Even if the common LTD plan’s target replacement level of 60% is achieved, 60% replacement still results in an income shortfall during a disability.

With higher medical expenses incurred during a disability, coupled with the higher cost of living in today’s inflationary environment, consider offering a Supplemental Disability Insurance plan that can protect up to 75% or 80% of pre-disability earnings.

Supplemental Disability Insurance can cover total compensation, is fully portable, offered on a Guarantee Issue basis, easy to install, can be employer-paid or voluntary, and is a very affordable benefit.

May is Disability Insurance Awareness Month (DIAM), and it is a suitable time to explore offering this benefit program.

Navis Benefits Group, LLC specializes in Supplemental Disability Insurance plans, and can help you design, market, install, and administer the plan.

The Missing Fourth Pillar - Financial Wellness

For most Employers, the financial wellness of their employees is a front and center priority.

The four pillars of an Employer’s financial wellness strategy should include protecting the ability to earn an income when disabled; providing the opportunity to save for retirement; extending an income lifeline to the employee’s beneficiaries in the event of death; and preserving accumulated assets in the event of a long-term care event.

Income Protection (STD/LTD/IDI), 401k, and Life Insurance are commonly offered benefits. These benefits address three pillars of a financial wellness strategy.

A long-term care event is perhaps one of the greatest threats to one’s accumulated assets, and the odds of financial exposure are greater than that of a disability.

Until recently, Employers haven’t had a viable solution for the fourth pillar: asset preservation in the event of a long-term care event.

Benefit and Human Resource Benefit Professionals practicing in the late 1990s will remember the surge in popularity for Group Long-Term Care Benefit programs. GLTC programs saw its peak as the most popular benefit program between 1996 and 2010, primarily due to favorable tax legislation introduced in 1996 and the ability to secure coverage on a guaranteed issue basis. By 2012, the leading GLTC insurance companies abandoned the new sales of GLTC products, recognizing too late that the product was underpriced, and the risk assumed would be costly.

Today’s asset preservation solution is better than ever. Known as “Hybrid” products, this innovative benefit combines permanent life insurance, with long-term care protection.

What is a Hybrid Product?

Offers “two-in-one” protection, with bundled Permanent Life Insurance and Long-Term Care Benefits

Permanent Life Insurance provides:

Death benefit

Cash Accumulation

Ability to take a loan against the policy

Long-Term Care (LTC) Benefits provides:

Accelerated funds from the Life Insurance policy, in the event of a LTC event

Benefit can be paid monthly, or via single lump sum

Funds are used to pay for care at home or in a skilled facility

Limits the need for insured to “tap into savings” or sell assets, to fund costly LTC.

What is Long-Term Care?

The care required when someone is unable to take care of themselves, due to a loss of 2 or more activities of daily living (ADLs) or if suffering from severe cognitive impairment.

ADLs include bathing, dressing, eating, toileting, transferring, continence

Severe Cognitive Impairment includes Alzheimer’s, Parkinson’s, dementia, or brain trauma.

Care can be provided in a skilled nursing facility, or at one’s home often by a licensed professional

Cost of Long-Term Care (LTC) Services?

Generally, not paid for by Disability, Medicare, or Health Insurance

Medicaid only pays once assets are depleted

Cost for LTC services is expected to double by 2051

The current cost can exceed $10,000/month in the Northeast

The average duration of care received is between 3 to 4 years

Resulting financial exposure ranges from $360,000 to $480,000

Only 1/3 of Americans have set aside money to protect themselves should the need arise

In the absence of LTC Insurance, a claim can quickly deplete assets including savings, retirement accounts, and even the home.

Why a Hybrid Product?

The benefit is a cornerstone to Financial Wellness, by providing 2-in-1 protection. Permanent Life insurance that can be taken into retirement, at the same cost, unlike Group Term Life Insurance. Valuable Long-Term Care coverage helps protect assets, by providing a source of funding the cost of care, rather than depleting savings, retirement accounts, or assets to pay for the cost of care.

Unlike GLTC plans once offered where the insured might not ever receive a benefit after years of paying premium, Hybrid products provide the opportunity to realize a return on investment by either collecting under the Life Insurance’s Death Benefit, or Long-Term Care provision. Also, unlike GLTC plans once offered, insurance carriers can’t file for state approved rate increases due to claims experience with Hybrid products.

Considering adding a new Hybrid Life/LTC Plan to your Employee Benefits?

Product design, underwriting offers, and plan pricing are important factors to consider.

Employee education and appropriate enrollment tools are crucial to the success of the program.

Most States require the Broker or Consultant meet specific Long-Term Care licensing requirements.

An Intelligent Investment

Employers can different themselves from their competitors, and strengthen their Financial Wellness Program, by adding a Permanent Life Insurance with Long-Term Care Benefit Program. Asset preservation is an important fourth pillar that, until recently, Employers haven’t had a solution for, since 2010.

This solution provides the ability for employees to realize a return on investment, by collecting under the life insurance’s death benefit, or the long-term care benefit. Coverage can be offered on a voluntary/payroll deduct or an employer-paid basis, secured on a guaranteed issue basis, and offered with affordable premiums. The coverage is portable in retirement, at the same premiums.

Most importantly, the absence of an asset protection pillar can place a substantial financial burden on employees, leaving employees and their families exposed to exorbitant cost of long-term care, and rapid asset depletion. A Hybrid program is an intelligent solution for asset preservation – the fourth pillar of a holistic Financial Wellness approach. A Hybrid Benefit Program provides valuable Long-Term Care coverage that can help protect assets, by offering a funding source for the cost of care, rather than depleting savings, retirement accounts, or assets to pay for the cost of care.

Trending “Executive” Benefit Alert!

Employer-paid Asset Protection, with Golden Handcuffs

Employers are always looking for new ways to improve their benefit program and retain top talent.

Retaining key employees, leveraging a golden handcuff type benefit, is nothing new. Employer-paid group long-term care (GLTC) programs were a huge hit in the 1990s - 2012, when all the largest providers left the market, and the industry died. Still, nothing new here.

So, what’s different and trending?

Employer-paid Permanent Life Insurance, with a Long-Term Care Rider, and fully paid up within 10 years. Yes, this benefit offering is one of the newest, and hottest, Executive Benefit Programs.

Why?

The employer can identify a class of key-employees, or Executives to exclusively offer the program to. As an employer-paid benefit, coverage can be secured on a true Guarantee Issue basis. Upon issuing coverage, the Permanent Life Insurance provides an instantaneous death benefit, and well as Long-Term Care Protection in the event of a long-term care event. As the employer pays premiums on behalf of the key employees, cash values accumulate. With an Accelerated Payment Option, such as 10-Pay, the Permanent Life policy’s premium can be fully paid-up within 10 years. After 10 years, the key employee(s) have their own fully paid-up permanent life insurance policy with a full death benefit, long-term care protection, and access to their policy’s cash value. The cash value can be leveraged to take loans, against the policy. Or the key employee has the option to surrender the policy and “cash the policy in” for the policy’s cash surrender value.

The 10-Pay helps the Employer retain top talent. Should the key employee leave before the 10-year period, the Employer has the option to stop funding the policy. Sure, the Executive port coverage with the accumulated values if they leave before the10 years. However, the key employee would be responsible for paying the higher accelerated option premiums until the plan is fully paid for. The longer the key employee stays with the Employer, the greater the accumulated cash value, and the less premium that remains to be paid.

Permanent Whole Life Insurance, with an LTC Rider, and paid for on a 10-Pay basis by the employer, is a resurrection of the old Group LTC plans, but better. These plans offer the guarantee that premiums will not increase once fully paid-up, unlike GLTC plans which have seen numerous rate increases. And unlike GLTC where no benefit is realized unless the insured collects for a long-term care loss, Permanent Whole Life with LTC Rider provides the possibility of a benefit for death, long-term care protection, and accumulated cash value.

Navis Benefits Group specializes in designing Employer-paid Permanent Life with Long-Term Care protection programs, on an Accelerated Payment Option basis. Ask how Navis Benefits Group can help you with this trending benefit.

Employer-paid Asset Protection, with Golden Handcuffs

Employers are always looking for new ways to improve their benefit program and retain top talent.

Retaining key employees, leveraging a golden handcuff type benefit, is nothing new. Employer-paid group long-term care (GLTC) programs were a huge hit in the 1990s - 2012, when all the largest providers left the market, and the industry died. Still, nothing new here.

So, what’s different and trending?

Employer-paid Permanent Life Insurance, with a Long-Term Care Rider, and fully paid up within 10 years. Yes, this benefit offering is one of the newest, and hottest, Executive Benefit Programs.

Why?

The employer can identify a class of key-employees, or Executives to exclusively offer the program to. As an employer-paid benefit, coverage can be secured on a true Guarantee Issue basis. Upon issuing coverage, the Permanent Life Insurance provides an instantaneous death benefit, and well as Long-Term Care Protection in the event of a long-term care event. As the employer pays premiums on behalf of the key employees, cash values accumulate. With an Accelerated Payment Option, such as a 10-Pay, the Permanent Life policy’s premium can be fully paid up within 10 years. After 10 years, the key employee(s) have their own fully paid-up permanent life insurance policy with a full death benefit, long-term care protection, and access to their policy’s cash value. The cash value can be leveraged to take loans, against the policy. Or the key employee has the option to surrender the policy and “cash the policy in” for the policy’s cash surrender value.

The 10-Pay, helps the Employer retain top talent. Should the key employee leave before the 10-year period, the Employer has the option to stop funding the policy. Sure, the Executive port coverage with the accumulated values if they leave before the 10 years. However, the key employee would be responsible for paying the higher accelerated option premiums until the plan is fully paid for. The longer the key employee stays with the Employer, the greater the accumulated cash value, and the less premium that remains to be paid.

Permanent Whole Life Insurance, with a LTC Rider, and paid on a 10-Pay basis by the employer, is a resurrection of the old Group LTC plans, but better. These plans offer the guarantee that premium will not increase once fully paid-up, unlike GLTC plans which have seen numerous rate increases. And unlike GLTC where no benefit is realized unless the insured collects for a long-term care loss, Permanent Whole Life with LTC Rider provides the possibility of a benefit for death, long-term care protection, and accumulated cash value.

Navis Benefits Group specializes in designing Employer-paid Permanent Life with Long-Term Care protection programs, on an Accelerated Payment Option basis. Ask how Navis Benefits Group can help you with this trending benefit.

Specialty Benefit Brokers complement the Employee Benefit Broker’s medical insurance expertise.

Specialty Benefit Brokers complement the Employee Benefit Broker’s medical insurance expertise.

With over 29 years of experience in specialty benefit solutions, Navis Benefits Group is well positioned to help Employee Benefit Brokers, and their Employers successfully compete for top talent with better benefits.

By focusing only on non-medical benefits, Specialty Benefits brokers are in the best position to partner with Employee Benefit Brokers and Employers on their STD, LTD, Life, Executive Benefits, and Worksite Benefit programs.

Navis Benefits Group partners with Employee Benefit Firms that focus on medical insurance, as their independent outsourced “specialty benefits” firm. We help them diversify the range of products and services they offer to their clients, without the need to hire an internal specialist to bring intelligent and creative non-medical benefit solutions to their Employer clients.

Navis Benefits Group helps Employers upgrade their benefit plans to a more state-of-the-art, competitive benefit program by identifying benefit gaps over-looked due to the heavy focus on medical insurance. We benchmark existing STD/LTD/Life, Voluntary Worksite, and Executive benefit plans; and we provide better benefit solutions.

We’ve worked with Employers of all sizes and industries and have helped solve some of the most complex problems.

Reach out to Navis Benefits Group, to see how we can help.

With over 29 years of experience in specialty benefit solutions, Navis Benefits Group is well positioned to help Employee Benefit Brokers, and their Employers successfully compete for top talent with better benefits.

By focusing only on non-medical benefits, Specialty Benefits brokers are in the best position to partner with Employee Benefit Brokers and Employers on their STD, LTD, Life, Executive Benefits, and Worksite Benefit programs.

Navis Benefits Group partners with Employee Benefit Firms that focus on medical insurance, as their independent outsourced “specialty benefits” firm. We help them diversify the range of products and services they offer to their clients, without the need to hire an internal specialist to bring intelligent and creative non-medical benefit solutions to their Employer clients.

Navis Benefits Group helps Employers upgrade their benefit plans to a more state-of-the-art, competitive benefit program by identifying benefit gaps over-looked due to the heavy focus on medical insurance. We benchmark existing STD/LTD/Life, Voluntary Worksite, and Executive benefit plans; and we provide better benefit solutions.

We’ve worked with Employers of all sizes and industries and have helped solve some of the most complex problems.

Reach out to Navis Benefits Group, to see how we can help.

Why Partner with a Specialty Benefits Broker?

Non-Medical Case Study

I. Employee Benefit Brokers focus attention heavily on Health Insurance. Why?

a. One of the highest budgetary items for Employer. It is a “must” priority.

b. Highest revenue generating product of all employee benefits for Employee Benefit Broker.

II. This is problematic for non-health insurance benefits, which are often neglected year after year.

a. STD/LTD/Life Renewals are often “rubber-stamped” given the smaller budget scale to health insurance, and limited Employee Benefit Broker shelf space.

i. This has a compounding effect on the cost of these benefits over the year.

b. Benefits can become stagnant. Result:

i. Ancillary benefit provisions are not modernized enough to meet today’s diverse workforce, do not include new creative benefit provisions, are not in alignment with the market, and are overpriced.

ii. Specialty Benefits such as Executive Benefits, Voluntary Benefits, and Long-Term Care benefits are last in line; designed poorly; or ignored completely.

III. Specialty Benefit Brokers complement the Employee Benefit Broker’s health insurance expertise.

a. By focusing only on non-medical benefits – Specialty Benefits brokers are in best position to partner with Employee Benefit Brokers and Employers on STD, LTD, Life, Executive Benefits, and Worksite Benefit programs.

Non-Medical Case Study:

Ø The Employer had been with the same Employee Benefits Broker for 20+ years.

o Employer also with the same Group LTD/Life Insurance company for 20+ years

o No rate decreases in at least several years, was a strong indicator to the Specialty Benefit Broker that LTD/Life plans had not been market evaluated.

o Antiquated Group LTD and Group Life plan designs were not in alignment with the market.

Ø A competing Employee Benefits Broker with the Employer, partnered with Navis Benefits Group to “test” the ancillary market and provide modernized solutions. Results:

o Demonstrated Employer had been paying too much for Group LTD and Group Life - 2x market!

§ Provided 50% savings with same plan designs from current plans.

o Provided alternative plan designs with modernized provisions at 49% savings from current. Stronger benefit provisions with higher net benefits!

§ Life: Doubled GI face amounts from 2x to 250k, to a 2x to 500k plan.

§ LTD:

· Increased benefit maximum from $10,000 to $12,500/month

· Improved after tax/net benefit from 50.4% to 65%.

o Helped Employer fill benefit plan gaps with ancillary savings:

§ Group STD: replaced fully insured program with enhanced self-insured.

§ Executive Disability Insurance: